UK Customs Declaration Errors: Top 10 Mistakes & How to Avoid Them

- John Hall

- Customs Specialist at iCustoms.ai

Every agent fears the same thing: one costly slip on an entry. Knowing the main UK customs declaration errors how to avoid them is the best protection against HMRC penalties, delays, and seized goods. This guide takes a problem-solution approach. It walks through the ten most common customs declaration mistakes UK agents make, explains why each one hurts, and shows how to stop it. Read it as a checklist you can apply to every declaration you file.

Why customs declaration errors are so costly

A customs error is rarely a small problem. When a declaration is wrong, HMRC can act in several ways at once, and the costs add up fast. That is why prevention beats correction every time.

The real cost of a mistake

The consequences reach well beyond a corrected form. In practice, a single error can trigger the following:

- Civil penalties for customs contraventions

- A post-clearance demand (C18) for underpaid duty and VAT

- Delays and storage charges while goods are held at the border

- A higher chance of HMRC audits and future checks

- Lost trust with the client whose goods are stuck

Put together, these customs declaration mistakes UK agents dread can turn a routine shipment into a costly, stressful problem. Fortunately, almost all of them are avoidable.

It is worth being clear about how penalties work. HMRC can issue civil penalties for customs contraventions, and it can reclaim underpaid duty and VAT through a post-clearance demand. Repeated or careless errors attract more scrutiny, whereas a clean record and quick corrections count in your favour. In short, the way you handle an error matters as much as the error itself.

Why agents carry the risk

As the party filing, you sit close to the liability, especially under indirect representation. Even under direct representation, a client whose goods are stuck will look to you first. Therefore, error prevention protects your business, not only the declaration.

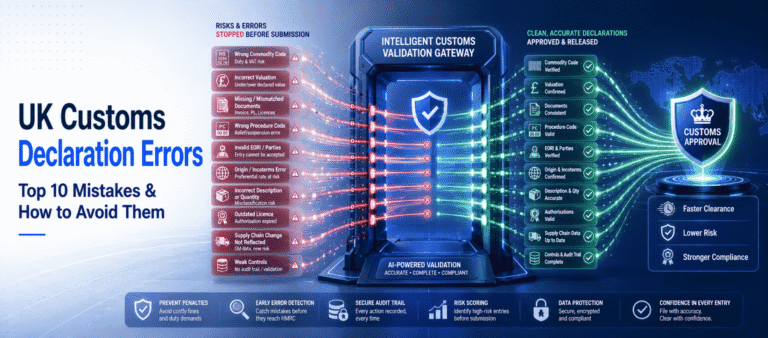

The top 10 UK customs declaration errors and how to avoid them

Below are the ten errors we see most often, with a practical fix for each. Work through them, and you remove the biggest risks in one pass.

Together, these are the UK customs declaration errors how to avoid first, since they cause the most damage and the biggest bills.

1. Wrong commodity code

The most common and expensive error is the wrong commodity code. A single wrong digit can change the duty rate, the VAT, and any licence requirement. To avoid it, classify carefully against the current UK Trade Tariff, and use classification support rather than guessing or copying an old entry.

2. Incorrect customs valuation

HMRC expects the correct customs value, usually the transaction value plus certain costs such as freight and insurance. Using the wrong valuation method understates or overstates the duty due. To avoid it, apply the correct method and keep the invoice and cost evidence to back it up.

3. Missing or mismatched documents

Entries fail when documents are missing or do not match the declaration. A gap between the invoice, the packing list, and the entry invites a query. To avoid it, check that every figure lines up before you submit, and keep licences and certificates ready.

4. The wrong procedure code

Procedure codes tell HMRC what is happening to the goods. The wrong code can suspend duty that is actually due, or charge duty that should be relieved. To avoid it, pick the code that matches the movement and verify it. Our procedure codes guide explains how.

5. Misunderstanding rules of origin

Origin decides preferential duty rates under trade agreements. Misunderstanding the rules of origin leads to wrongly claimed preference and later demands. To avoid it, confirm the origin rules for the goods and hold valid proof of origin before you claim.

6. Getting Incoterms wrong

Incoterms set who carries the cost and risk, and they affect the customs value. Getting them wrong distorts both the valuation and the paperwork. To avoid it, confirm the agreed Incoterm on every shipment and reflect it correctly on the entry.

7. Incorrect goods descriptions and quantities

Vague descriptions and wrong quantities cause queries and mis-classification. A description such as ‘parts’ tells HMRC very little. To avoid it, describe goods precisely and check quantities against the packing list.

8. Invalid EORI or party details

An invalid or expired EORI, or the wrong party details, stops an entry cold. To avoid it, confirm the importer, exporter, and representation details before filing, and check that the EORI is active.

9. Ignoring supply chain changes

Supply chains change: new suppliers, new routes, new terms. Reusing an old template after a change bakes the error straight in. To avoid it, review the entry whenever the supplier, origin, or Incoterm changes, rather than copying last time’s data.

10. Weak internal controls and no technical back-up

Finally, many mistakes trace back to weak internal controls and no technical back-up. Without checks, validation, and an audit trail, errors slip through and repeat. To avoid it, build a review step into every filing and use software that validates entries and records exactly what was filed.

Other mistakes to watch

Beyond the top ten, a few smaller errors still cause trouble. Keep an eye on these:

- Duty or VAT paid through the wrong account, or an account with no funds

- Missing the supplementary declaration deadline on simplified entries

- Currency and exchange-rate errors in the customs value

- Outdated licences or expired authorisations

None of these is exotic, yet each one still holds up goods. A final review usually catches them before they cause a problem.

How software prevents these errors

Most CDS submission errors are preventable. iCDS validates every declaration before it reaches HMRC, checks commodity codes, and flags mismatches between your documents and your data. As a result, errors are caught at your desk rather than at the border. Moreover, it keeps a clear record of every entry, which strengthens your internal controls.

In practice, that automation covers the errors above in a few ways:

- Automatic validation of mandatory data elements

- Commodity code and procedure code checks

- Alerts for missing documents or mismatched values

- A full audit trail for every declaration you file

Crucially, prevention is cheaper than correction. Every error caught before submission is one that never becomes a penalty, a delay, or an awkward call with a client.

What to do if you spot an error

Mistakes still happen, so know the fix. If you spot an error after submission, act quickly. First, correct the entry through an amendment where the goods are still in scope. Next, if duty or VAT was underpaid, make a voluntary disclosure to HMRC rather than waiting for a demand. Finally, record what went wrong and adjust your process so it does not repeat.

Prompt, honest correction usually reduces any penalty and shows HMRC that your controls work. That is far better than hoping an error goes unnoticed.

Checklist for agents

Before you submit any entry, run this quick checklist. It takes minutes, yet it removes the errors that cause most penalties:

- Confirm the commodity code against the current tariff

- Check the customs value and the valuation method

- Match the invoice, packing list, and entry

- Verify the procedure code and additional procedure code

- Confirm origin and hold valid proof

- Check the Incoterm and how it affects value

- Confirm the EORI and party details are valid

- Review for any supply chain changes

- Run a validation check before submission

- Keep a record of exactly what was filed

Used on every entry, this list is the simplest guide to UK customs declaration errors how to avoid before HMRC ever sees a problem.

Frequently Asked Questions

What are the most common UK customs declaration errors?

The most common are wrong commodity codes, incorrect valuation, missing documents, and the wrong procedure code. Each can trigger delays, penalties, or a duty demand.

What happens if I make a customs declaration mistake?

HMRC can charge civil penalties, issue a post-clearance demand for underpaid duty and VAT, and hold the goods. In serious cases, it may seize them.

How can I avoid CDS submission errors?

Validate every entry before you submit, check documents against the data, and use software that flags errors early. A pre-submission checklist helps too.

Can I correct a customs declaration after submission?

Yes. You can amend an entry or make a voluntary disclosure to HMRC. Acting quickly usually reduces the penalty and shows good compliance.

Who is responsible for a customs declaration error?

It depends on the representation type. Under direct representation the importer usually carries liability, while indirect representation shares it with the agent.

How much are HMRC customs penalties?

Penalties vary with the contravention and whether it was careless or deliberate. HMRC can also reclaim underpaid duty and VAT, so the total cost often exceeds the penalty alone.

Does software really reduce customs declaration errors?

Yes. Validation catches missing or mismatched data before submission, which removes many CDS submission errors that would otherwise reach HMRC.

You may also like:

Struggling to Extract, Catagorise & Validate Your Documents?

Capture & Upload Data in Seconds with AI & Machine Learning

Subscribe to our Newsletter

About iCustoms

iCustoms is an all-in-one solution helping businesses automate customs processes more efficiently. With AI-powered and machine-learning capabilities, iCustoms is designed to streamline your all customs procedures in a few minutes, cut additional costs and save time.

Struggling to Extract, Catagorise & Validate Your Documents?

Capture & Upload Data in Seconds with AI & Machine Learning