What Is a Safety and Security Declaration? The Complete UK and EU Guide (2026)

- Freya Jane

- Director of Customer's Success

Key Takeaways

A Safety and Security Declaration is a mandatory pre-arrival notification required by UK customs law and EU regulation for most goods entering the UK or EU.

In the UK it is called an Entry Summary Declaration (ENS) and is submitted via HMRC’s Customs Declaration Service (CDS).

In the EU it is governed by the Import Control System 2 (ICS2), which reached its final phase in 2024.

Non-compliance can result in civil penalties of up to GBP 2,500 per declaration in the UK and refusal of entry for goods.

Customs software like iCustoms connects directly to HMRC CDS and automates the entire ENS filing process, eliminating manual errors.

If your goods are heading into the UK or European Union, chances are you need to file a Safety and Security Declaration before they even leave the port of loading. This is not optional paperwork. It is a legal requirement designed to give customs authorities the information they need to carry out risk assessments before goods arrive.

This guide covers everything you need to know: what a Safety and Security Declaration is, who is responsible for filing it, how to submit it through HMRC CDS or EU ICS2, the deadlines that apply to each transport mode, what happens if you miss them, which goods are exempt, and how customs software can automate the process from end to end.

What Is S&S GB (Safety and Security Great Britain)?

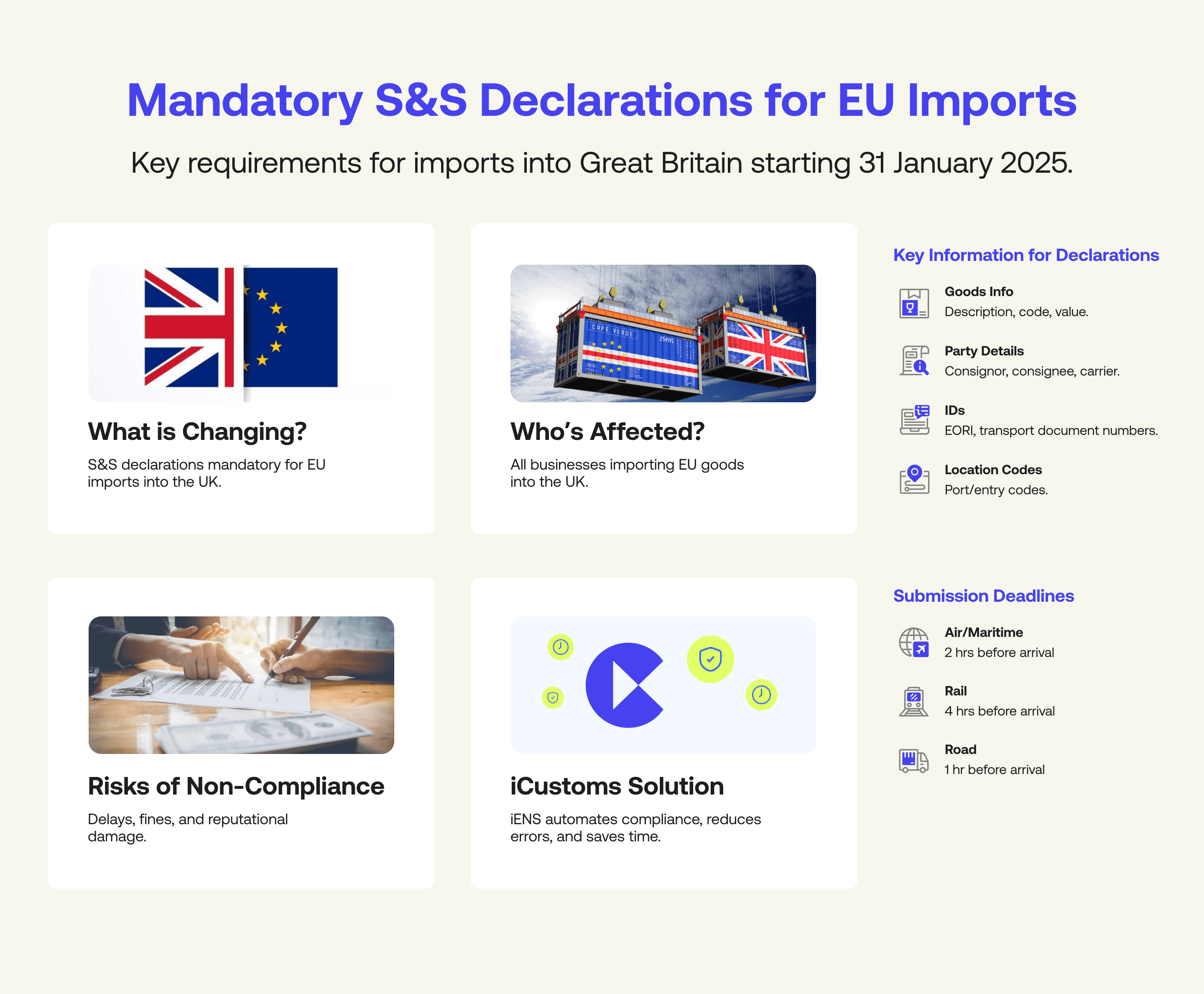

S&S GB stands for Safety and Security Great Britain. It is the name HMRC and UK trade professionals use to refer to the UK’s pre-arrival safety and security declaration regime for goods entering Great Britain. Under S&S GB, the carrier or their authorised representative must submit an Entry Summary Declaration to HMRC before the goods arrive at a UK port or airport.

The S&S GB regime came into full operation at the end of the Brexit transition period. Before Brexit, UK businesses moving goods within the EU were not required to file ENS declarations for intra-EU movements. Post-Brexit, all goods entering Great Britain from abroad, including from EU member states, are subject to S&S GB requirements. Northern Ireland operates under different arrangements as part of the Windsor Framework.

The ENS submitted under S&S GB is processed by HMRC’s Customs Declaration Service, which conducts an automated risk assessment on the declared goods. If the system flags a consignment, HMRC may issue a ‘do not load’ instruction before departure or a hold on the goods upon arrival. The ENS generates a Movement Reference Number upon successful submission. This MRN must be communicated to the carrier and presented at the border.

S&S GB Declaration Deadlines by Transport Mode

The deadline by which an ENS must be submitted before goods arrive in Great Britain depends on the mode of transport. Missing these deadlines is treated the same as not filing at all and carries the same penalties. The deadlines below are set by HMRC under the S&S GB rules.

| Mode of Transport | ENS Filing Deadline | Practical Implication |

|---|---|---|

| Deep-sea container shipping | 24 hours before loading at the port of departure | Longest lead time in the system. The ENS must be filed before the container is loaded onto the vessel, not before the vessel departs. For cargo with multiple transhipment legs, this applies at the first port of loading. |

| Short-sea and RoRo shipping | 2 hours before arrival at the UK port | Applies to roll-on roll-off ferry services. The shorter window reflects faster transit times. For regular ferry routes (Dover to Calais, Holyhead to Dublin), operators and their agents must have automated filing systems in place. |

| Air cargo (long haul) | 4 hours before arrival at the UK airport | Applies to long-haul air freight where the flight time exceeds 4 hours. Express courier consignments may have different rules under express carrier procedures. |

| Air cargo (short haul) | As early as practicable; minimum at departure | Applies to short-haul flights of under 4 hours. Declaration must be submitted no later than the moment of aircraft departure. |

| Rail freight and Eurotunnel | 2 hours before arrival at the first UK rail terminal | Applies to cross-Channel rail services including Eurotunnel freight shuttle. The 2-hour window matches the RoRo window given similar transit characteristics. |

| Road freight | 1 hour before arrival at the UK border | The shortest window in the system. Road hauliers and their agents must have rapid-filing capabilities. Under GVMS, the ENS MRN must also be included in the Goods Movement Reference before the vehicle boards. |

Note: Under GVMS (Goods Vehicle Movement Service), the ENS MRN must be added to the vehicle’s Goods Movement Reference (GMR) before the vehicle boards the ferry or enters the Eurotunnel terminal. A vehicle arriving at Dover or Holyhead without a valid GMR that includes all required MRNs will be refused boarding. This is the most common cause of freight delays at major UK RoRo ports.

Start automating your Safety and Security Declarations today.

iCustoms integrates with HMRC CDS and handles ENS filing automatically. No setup fees. No long contracts. Start your free trial now.

Goods Exempt from S&S GB and Safety and Security Declarations

Not all goods entering Great Britain require an ENS under S&S GB. HMRC has published the full list of exemptions in Public Notice 760. The most common exempt categories are set out below. If you are unsure whether your goods qualify for an exemption, seek advice from a qualified customs agent before assuming an exemption applies. Incorrectly claiming an exemption and not filing is treated as non-compliance.

- Goods brought into Great Britain from a country that has a bilateral security and safety agreement with the UK providing for mutual recognition of pre-arrival controls.

- Goods carried as personal effects by passengers travelling for non-commercial purposes.

- Goods in postal consignments with a value below GBP 135 that are not subject to prohibitions or restrictions (express courier shipments have separate rules and are not covered by this exemption in all cases).

- Military goods and goods for the armed forces travelling under military transport arrangements.

- Goods covered by diplomatic bags under the Vienna Convention on Diplomatic Relations.

- Goods in temporary storage not exceeding 45 days at an approved temporary storage facility.

- Goods moving between Great Britain and the Channel Islands or the Isle of Man under specific arrangements.

Penalties for Not Complying with S&S GB Requirements

HMRC takes non-compliance with S&S GB obligations seriously. The penalty regime is set out under Schedule 41 of the Finance Act 2008 and applies across four scenarios.

Failure to submit an ENS at all carries a civil penalty of up to GBP 2,500 per declaration. Persistent non-compliance can result in escalating penalties and referral to HMRC’s criminal investigation unit.

Submitting after the deadline, even if the ENS is eventually submitted, carries a reduced penalty of GBP 500 which rises on a sliding scale for repeated late filings.

Submitting with inaccurate or incomplete data, such as an incorrect HS code, wrong EORI number, or missing container reference, carries a penalty of up to GBP 2,500. The risk assessment system may also place a hold on the goods until the inaccuracy is resolved.

Beyond financial penalties, goods may be refused entry or placed in temporary storage at the importer’s cost. Storage charges at major UK ports including Felixstowe, Tilbury, and Southampton can run to several hundred pounds per day, rapidly exceeding the maximum financial penalty.

A single rejected ENS at Felixstowe or Dover can cost thousands of pounds in storage charges, missed delivery windows, and staff time, far exceeding the GBP 2,500 maximum penalty. Automated customs software that validates ENS data before submission is the most cost-effective compliance investment available for any business moving goods into Great Britain.

GVMS and S&S GB: How the Goods Movement Reference Links Declarations

Safety and security obligations apply to exports as well as imports. The Exit Summary Declaration, known as an EXS, must be submitted when goods leave Great Britain by road or rail, or when there is no export declaration that already covers the required safety and security data fields.

The EXS is submitted via HMRC CDS after the export declaration has been accepted but before the goods physically leave Great Britain. It generates a separate MRN number confirming the safety and security data for the outgoing goods. For many export movements, the data required for an EXS is already captured within the export declaration itself, in which case a standalone EXS is not required. For goods moving under transit procedures or where the export declaration does not cover all safety and security fields, a separate EXS must be filed.

T1 Transit Declarations and the Transit Accompanying Document

When goods move through multiple customs territories without entering free circulation, they travel under a transit procedure. The most widely used procedure for UK and EU movements is the Common Transit Convention (CTC), processed electronically via the New Computerised Transit System (NCTS), currently operating at Phase 5.

A T1 transit declaration applies to goods that have not been cleared through customs. The T1 declaration is submitted electronically via NCTS and generates an MRN. The Transit Accompanying Document (TAD) is the printout or electronic record of the transit declaration that travels with the goods. The TAD must be presented at the office of transit and the office of destination.

In most cases, goods moving under a T1 transit procedure do not require a separate ENS because the transit declaration covers the necessary safety and security data. However, the interaction between transit procedures, S&S GB obligations, and GVMS requirements can be complex at border crossings where transit and import procedures coincide.

Skip the manual process entirely.

iCustoms connects directly to HMRC CDS and files your Safety and Security Declarations automatically, with built-in data validation to prevent costly rejections. Book a free 15-minute demo to see it in action.

How iCustoms Automates S&S GB, ENS, ICS2 and PLACI Filings

Filing S&S GB Entry Summary Declarations manually through HMRC CDS is time-intensive, requires detailed knowledge of data requirements, and carries a high error rate under time pressure. For businesses operating across multiple transport modes or handling high shipment volumes, manual filing is not viable. iCustoms was built to remove this complexity.

| Without iCustoms | With iCustoms |

|---|---|

| Manual data entry into HMRC CDS portal, repeated for every shipment | Automated ENS data population from trade documents, saved consignor and consignee profiles, and template-based filing |

| No pre-submission validation; errors discovered only after HMRC rejection | Built-in validation checks before submission: EORI format, commodity code structure, container reference format, transport data completeness |

| Manual tracking of MRNs across multiple shipments and transport modes | Centralised MRN management dashboard showing status of every ENS, import, and transit declaration |

| Missed filing deadlines when manual processes are delayed | Automated deadline alerts by transport mode: 24-hour, 4-hour, 2-hour, and 1-hour pre-arrival reminders |

| No automated GVMS GMR population; MRNs must be entered manually into GVMS | iCustoms auto-populates the GMR with all relevant MRNs including the ENS MRN, eliminating manual GVMS entry |

| ICS2 and PLACI filed through a separate EU system with no connection to UK filings | iAIS handles ICS2 declarations and PLACI pre-loading notifications for EU air cargo movements from the same platform |

| T1 transit declarations managed separately via NCTS, no integration with ENS workflow | iNCTS handles T1 declarations via NCTS Phase 5, integrated with the broader iCustoms declaration management system |

| No audit trail; HMRC compliance reviews require manual reconstruction of filing history | Full submission log of every declaration, amendment, HMRC query, and system response, with timestamps and operator records |

| Updates to HMRC CDS data requirements require manual process changes | Automatic regulatory updates rolled out by the iCustoms platform team; no IT work required from the customer |

iCustoms integrates directly with HMRC’s CDS REST API for S&S GB ENS filing. iWiz handles automated import declarations. iAIS manages ICS2 and PLACI submissions for EU air cargo. iNCTS covers T1 and NCTS Phase 5 transit declarations. All products are available without setup fees, without long contracts, and with a free trial.

S&S GB Software: What to Look for When Evaluating Platforms

If you are evaluating S&S GB or ENS filing software for the first time, or considering switching from your current provider, the following criteria are the ones that matter most for operational reliability and compliance. A platform that cannot deliver on all of them will create risk and operational overhead rather than removing it.

| Capability | Why It Matters | iCustoms |

|---|---|---|

| Direct HMRC CDS API integration | API integration means declarations are filed in real time without manual portal access; no third-party intermediaries that can fail | Yes — direct REST API connection to HMRC CDS |

| Pre-submission data validation | Validation before submission catches errors before they cause HMRC rejections and border holds; critical for the 1-hour road window | Yes — commodity code, EORI, container reference, transport data all validated |

| All transport modes covered | Road 1 hour, RoRo 2 hours, air 4 hours, deep-sea 24 hours; software must handle deadline management across all modes | Yes — mode-specific deadline alerting for all 6 modes |

| GVMS GMR auto-population | For road and RoRo operators, automatic addition of ENS MRN to GMR eliminates the manual step most likely to cause boarding refusals | Yes — GMR auto-population from ENS MRN |

| ICS2 and PLACI support | For businesses with EU movements by air, ICS2 and PLACI compliance must be handled from the same platform | Yes — iAIS handles ICS2 H7 and H1 ENS including PLACI |

| NCTS transit support | For shipments moving under T1 transit, NCTS Phase 5 integration prevents separate manual filing | Yes — iNCTS handles T1 and NCTS Phase 5 |

| Multi-client management | Customs brokers and freight forwarders handling multiple clients need a dashboard that separates client data and filing history | Yes — multi-client dashboard with per-client audit trails |

| Audit log for HMRC compliance | Complete submission history with timestamps; essential for responding to HMRC queries and compliance reviews | Yes — full audit log of every submission, amendment, and HMRC communication |

| No setup fees, no minimum contract | Pricing transparency; especially important for SME importers evaluating cost vs manual filing | Yes — transparent per-declaration pricing, no setup fees, no minimum commitment |

Exit Summary Declaration (EXS): What Exporters Need to Know

A Safety and Security obligation exists not just for imports but also for exports leaving the UK. The Exit Summary Declaration, known as an EXS, must be submitted when goods leave the UK’s customs territory by road or rail, or when goods are exported from the EU and there is no export declaration covering the safety and security data.

The EXS is submitted after the export declaration has been accepted and before the goods physically leave the UK. It confirms the safety and security data for the exiting goods and allows customs authorities to conduct exit risk analysis. Like the ENS, the EXS is submitted via HMRC CDS and generates an MRN.

In many export movements, the data required for an EXS is already captured within the export declaration itself. In these cases, a separate EXS is not required. However, for goods moving under transit procedures or where the export declaration does not cover all required safety and security fields, a standalone EXS is necessary.

T1 Transit Forms and the Transit Accompanying Document (TAD)

When goods move through multiple customs territories without entering free circulation, they travel under a transit procedure. The most common transit procedure used for UK and EU movements is the Common Transit Convention (CTC), which uses the New Computerised Transit System (NCTS) for electronic declaration processing.

A T1 form is the transit declaration for goods that have not been cleared through customs and are therefore moving as ‘non-union goods’ (in EU terminology) or ‘non-UK duty-paid goods’ through the customs territory. The T1 declaration is submitted electronically via NCTS and generates a Movement Reference Number.

The Transit Accompanying Document (TAD) is the physical printout or electronic representation of the NCTS transit declaration that accompanies the goods during their journey. The TAD contains the MRN, a barcode, and the key details of the transit movement. It must be presented to customs at the office of transit and the office of destination.

For safety and security purposes, goods moving under a T1 transit procedure do not require a separate ENS in most cases because the transit declaration itself covers the safety and security data. However, the interaction between transit procedures, ENS obligations, and GVMS requirements can be complex, particularly for movements that combine transit and import procedures at the same border crossing.

Frequently Asked Questions About Safety and Security Declarations

The following questions are the most frequently searched topics related to Safety and Security Declarations. These should be marked up with FAQ schema in your CMS.

What is a Safety and Security Declaration?

A Safety and Security Declaration is a mandatory pre-arrival or pre-departure customs notification that provides information about goods entering or leaving a customs territory. In the UK, it is called an Entry Summary Declaration (ENS) and is submitted via HMRC's Customs Declaration Service. In the EU, it is governed by the Import Control System 2 (ICS2). Both systems use the data for risk analysis and security purposes.

What is the difference between a UK ENS and an EU ICS2 declaration?

The UK ENS is required for goods entering Great Britain and is submitted to HMRC via CDS. The EU ICS2 applies to goods entering the EU customs territory and is submitted to the relevant EU member state customs authority. Since the UK left the EU, both obligations can apply to the same shipment: one ENS for the UK leg and one ICS2 declaration for the EU leg if the goods transit through or enter the EU.

Who is responsible for submitting the Safety and Security Declaration?

The primary responsibility lies with the carrier: the person operating the means of transport that brings the goods into the customs territory. Carriers can delegate this to a customs representative, freight forwarder, or customs broker, who acts either as a direct or indirect representative. Importers who arrange their own freight may also be required to file if they have taken on the carrier's obligations contractually.

What are the deadlines for submitting a Safety and Security Declaration?

Deadlines vary by transport mode. For deep-sea container shipping, the ENS must be filed 24 hours before loading at the port of departure. For RoRo/short-sea shipping, the deadline is 2 hours before arrival at the UK port. For long-haul air cargo, it is 4 hours before arrival. For road freight, the deadline is 1 hour before arrival at the UK border. Rail freight requires submission 2 hours before arrival at the first UK rail terminal.

What are the penalties for not submitting a Safety and Security Declaration?

Under Schedule 41 of the Finance Act 2008, HMRC can issue civil penalties of up to GBP 2,500 per declaration for failure to submit an ENS. Submissions with material inaccuracies also attract penalties up to GBP 2,500. Beyond fines, non-compliant goods can be held at the border, incurring significant storage costs that often exceed the penalty itself.

Which goods are exempt from Safety and Security Declaration requirements?

Common exemptions include personal baggage carried by passengers, diplomatic goods under the Vienna Convention, military goods under military transport arrangements, and postal consignments below the GBP 135 value threshold that are not subject to prohibitions. Some goods covered by bilateral security agreements between the UK and third countries may also be exempt. Consult HMRC Public Notice 760 for the full and current list of exemptions.

How does GVMS interact with Safety and Security Declarations?

The Goods Vehicle Movement Service (GVMS) is HMRC's pre-lodgement system for road vehicles at UK ports. When GVMS applies, the carrier must create a Goods Movement Reference (GMR) before the vehicle arrives at the port and add the MRNs from all relevant declarations to it, including the ENS MRN. Vehicles arriving without a valid, complete GMR will be refused boarding or denied entry at GVMS-enabled ports.

Can customs software automate Safety and Security Declaration filing?

Yes. Customs software platforms like iCustoms connect directly to HMRC CDS via the official API and can automate the entire ENS filing process: from data capture and validation through to submission, MRN retrieval, and GVMS GMR population. This eliminates manual data entry errors, ensures deadline compliance, and provides a full audit trail for HM

You may also like:

Simplify Customs with our Powerful Customs Management Software

Automate declarations, track shipments, & ensure compliance.

About iCustoms

iCustoms is an all-in-one solution helping businesses automate customs processes more efficiently. With AI-powered and machine-learning capabilities, iCustoms is designed to streamline your all customs procedures in a few minutes, cut additional costs and save time.

Simplify Customs with our Powerful Customs Management Software

Automate declarations, track shipments, & ensure compliance.