Manual Product Classification, Not IOSS Drives EU Customs Compliance Risk after July 2026

- John Hall

- Customs Specialist at iCustoms.ai

The upcoming 1 July 2026 implementation of the €3 customs duty per tariff sub-heading has intensified scrutiny on EU low-value imports. Much attention focuses on IOSS as the disruption source. In reality, compliance exposure stems from manual product classification accuracy and cross-system customs data consistency, creating a growing manual classification compliance risk for importers. EU IOSS centralised VAT reporting but did not simplify tariff classification, origin checks, or customs data alignment.

The Real Pressure Point Behind €3 Customs Rule for Low-Value EU Imports

The scale of EU trade explains why the €3 Customs Rule makes classification precision more critical than ever. In 2024, bilateral EU–China trade reached €732 billion, with EU imports from China alone amounting to €519 billion, of which manufactured goods accounted for 96.7%. When such trade volumes enter a digitally monitored customs environment governed by the €3 customs duty rule, classification inconsistencies no longer remain marginal, they become statistically detectable compliance risks.

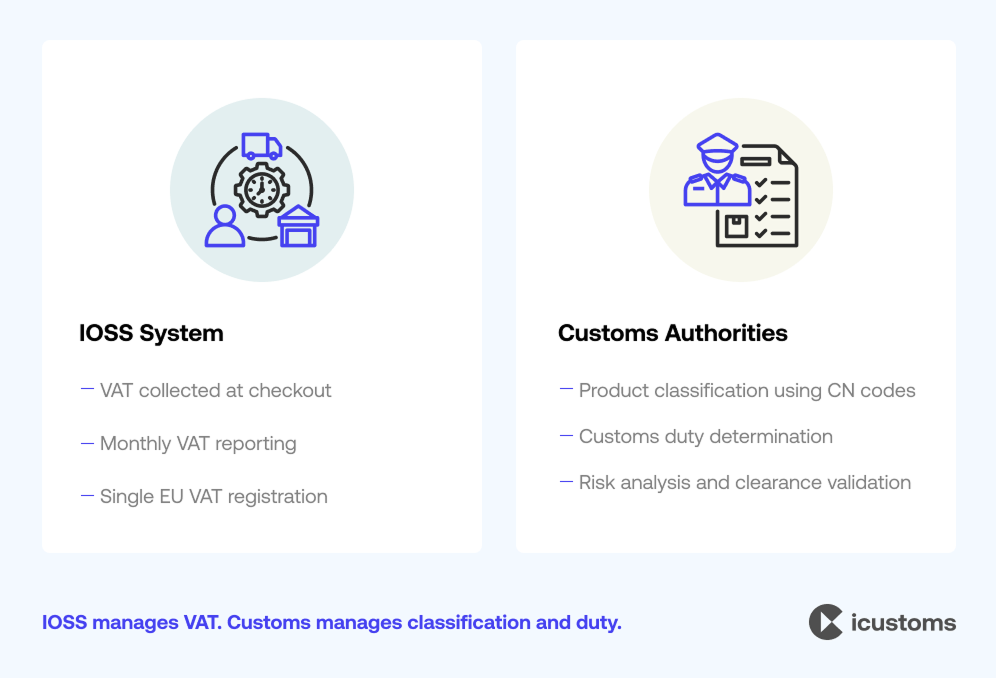

IOSS Centralises VAT. Customs Enforcement Operates Independently.

The Import One Stop Shop was introduced to reduce VAT fragmentation across 27 Member States. It allows sellers to collect VAT at checkout and submit a single monthly return, eliminating multiple VAT registrations. From a commercial standpoint, it enhances pricing transparency and reduces delivery friction.

However, IOSS for low-value EU imports addresses fiscal reporting, not customs logic. It does not alter tariff codes, duty exposure, trade defence measures, or origin-based restrictions. These remain governed by the EU Customs Code and national customs systems.

EU Customs Reform Is Shifting Toward Centralised Data-Driven Enforcement

While VAT became centralised, EU Customs Reform is shifting enforcement toward structurally integrated, data-driven control. The forthcoming EU Customs Data Hub (expected 2028) will centralise customs data processing and harmonise risk profiling across Member States, reflecting the EU’s strategic objective to strengthen tariff enforcement through unified digital infrastructure.

This reform emerges against a backdrop of structural trade imbalance. The EU recorded a €305.8 billion trade deficit with China in 2024, with the volume deficit rising to 44.5 million tons. Policymakers have openly positioned customs modernisation as a mechanism to restore competitive balance, improve tariff collection accuracy, and ensure consistent enforcement across the Single Market.

In that environment, product classification depth becomes economically material, as tariff determination, risk analysis, and enforcement decisions increasingly depend on precise, structured customs data.

IOSS vs Customs Responsibilities

| Compliance Function | IOSS | EU Customs Authorities |

| VAT collection and reporting | Yes | No |

| Tariff classification (HS/CN codes) | No | Yes |

| Customs duty calculation | No | Yes |

| Customs clearance decisions | No | Yes |

| Risk analysis and enforcement | No | Yes |

Product Misclassification Is the Hidden Multiplier in E-commerce

In cross-border trade, product misclassification acts as a hidden cost multiplier that many online sellers fail to recognise. Most product listings are engineered for conversion rates, not customs compliance accuracy. Descriptions such as “fitness bundle”, “smart home kit”, or “premium lifestyle accessory” lack the material composition and technical specifications required for accurate tariff determination at the 8 and 10 digit CN levels.

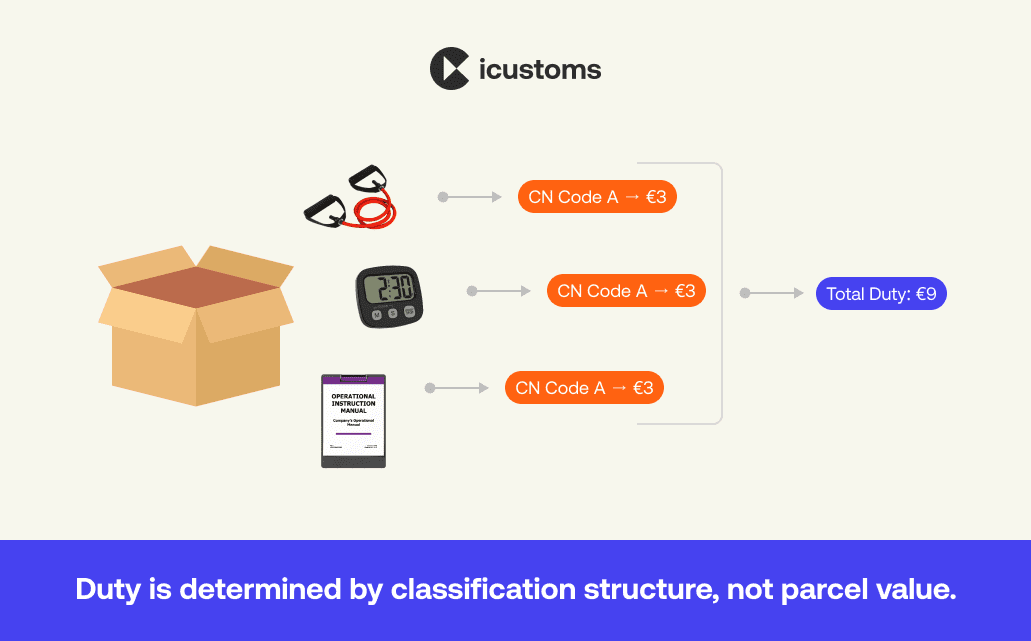

Consider a parcel containing:

• A resistance band set, a rubber-based product

• A digital workout timer, an electronic device

• A printed instruction manual, a paper product

Each item falls under a distinct tariff sub-heading. From a consumer perspective, this is one fitness package. From a customs perspective, it may represent three separate fiscal units requiring independent tariff classification. The seller sees one SKU, while customs authorities assess multiple classifications, increasing the risk of product misclassification, duty miscalculation, and regulatory scrutiny.

Incorrect Classification Creates Two Distinct Risks

The first risk is multiplication of interim €3 customs duties between 2026 and 2028. Because the €3 customs charge applies per tariff sub-heading, product classification structure directly determines duty exposure. Classification inconsistency can therefore increase customs duty without any change in product value or shipment volume.

The second and more structural risk is misclassification at extended digit level. If a resistance band is declared under a generic “sporting accessories” code rather than the correct rubber-based goods heading, duty treatment, statistical reporting, and potential trade measures may shift.

Repeated across thousands of low value parcels, small classification inaccuracies create measurable exposure. Under centralised data analysis, anomaly patterns are no longer invisible.

Cross-System Data Mismatch in Security Filings and Import Declarations

Low-value consignments entering the EU are subject to ICS2 Entry Summary Declarations prior to arrival. These filings include commodity descriptions, HS codes, and shipper data.

Once goods arrive, national customs systems assess the formal import declaration and any IOSS VAT reference. Where commodity wording, values, or classification depth diverge materially between ENS and import filings, systems may trigger validation queries or additional scrutiny.

The issue is not VAT miscalculation. It is structural data inconsistency that amplifies manual classification compliance risk across security filings and customs declarations.

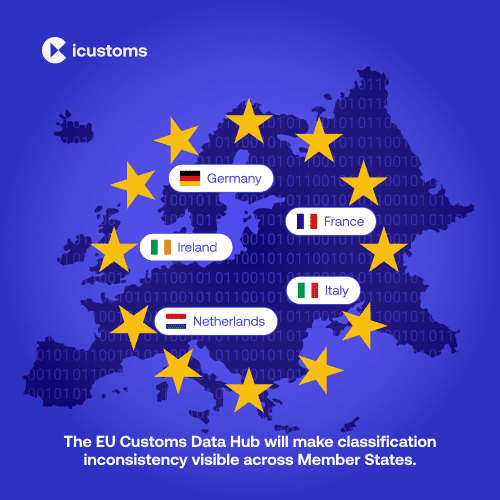

Data Hub Centralisation Will Amplify Variance

Today, inconsistencies may remain contained within a single Member State system. Under the EU Customs Data Hub, filing behaviour will increasingly be evaluated across jurisdictions.

If identical products are classified differently in Germany, Ireland, and the Netherlands, variance becomes visible at scale. In high-volume environments, particularly in electronics, automotive components, or consumer devices, statistical inconsistency can undermine release predictability. At scale, statistical inconsistency driven by manual classification compliance risk can undermine clearance predictability across multiple EU jurisdictions.

Data Pattern Monitoring as a Customs Risk Trigger

Enforcement is increasingly shifting from isolated inspection toward statistical pattern recognition across large datasets. Under the EU Customs Data Hub, classification inconsistency will no longer remain a localised administrative issue. It will become a visible, measurable customs risk indicator across EU Member States.

Duty Exposure Makes Classification a Commercial Liability

After July 2026, when per-sub-heading customs duty exposure becomes directly visible, logistics providers, customs brokers, and import operators will increasingly be required to justify classification outcomes to sellers and commercial partners. Classification decisions will directly influence duty liability, clearance predictability, and commercial accountability.

EU Imports Classification Risk After July 2026: Electronics and Modular Electronics

Certain sectors face elevated manual classification compliance risk, particularly where modular or multi-component goods complicate tariff treatment. EU imports of machinery and vehicles from China accounted for 55% of manufactured imports in 2024. Many low-value parcels now include modular electronics: cables, adapters, smart accessories, and peripheral devices.

These products often appear commercially interchangeable but fall under distinct tariff sub-headings. A charging dock, a lithium battery accessory, and a Bluetooth module may each carry separate classification logic. Incorrect bundling assumptions lead to unexpected duty multiplication.

Textiles, Multi-Material Goods, and Origin Sensitivity

Textile-based imports remain highly classification-sensitive due to fibre composition rules. A garment containing 60% polyester and 40% cotton may fall under a different heading than one reversed in composition.

If product listings omit material percentages, brokers must interpret from limited documentation. Under extended-digit CN logic, minor compositional differences alter classification outcomes. As tariff enforcement intensifies post-2026, documentation precision becomes commercially consequential.

Manual Classification Compliance Risk: Sellers vs Operators

E-commerce pricing models frequently assume simplified low-value treatment. When classification precision alters duty exposure, shipment partners become the intermediary between fiscal reality and commercial expectation.

This creates a subtle but growing tension between:

- Marketplace pricing assumptions

- Broker classification decisions

- Carrier cost recovery mechanisms

As a result, manual classification compliance risk increasingly shapes commercial accountability between sellers, brokers, and logistics intermediaries.

Customs Compliance Teams as Commercial Risk Interpreters

As enforcement deepens, customs departments are no longer back-office processors. They are becoming compliance strategists and dispute mediators. In an environment where EU imports exceeded $2.6 trillion in 2024, and China accounts for 22% of EU imports overall, regulatory scrutiny is aligned with macroeconomic policy.

Classification governance is not merely technical, it intersects with trade balance objectives and industrial policy concerns. The operational pressure will rise accordingly.

Strategic Conclusion: The Customs System Is Working, The Data Is Not

EU IOSS is functioning as intended. It centralises VAT and improves consumer transparency. What is destabilising EU imports is the mismatch between commercial product data and customs classification depth within an increasingly centralised digital enforcement ecosystem. This systemic gap elevates manual classification compliance risk from an operational issue to a strategic compliance priority.

Between 2026 and 2028, the interim €3 rule introduces visible fiscal sensitivity at sub-heading level. From 2028 onward, the abolition of the €150 exemption embeds low-value imports fully into the EU’s structured tariff framework.

Accuracy and Consistency is Key for Customs Systems

For brokers, forwarders, and customs operators, the decisive capability is no longer speed alone. It is structured, defensible, consistent classification governance that withstands statistical scrutiny across VAT, security, and customs systems. That is where the real EU customs import risk will emerge after July 2026, as classification accuracy becomes the decisive enforcement variable, not IOSS. Reducing manual classification compliance risk will become a defining capability for customs intermediaries operating in the post-2026 enforcement environment.

Eliminate Manual Classification Risk in EU Customs

Automate product classification, ensure CN accuracy, and maintain consistent EU customs data after IOSS reform.

Frequently Asked Questions

Is EU IOSS causing customs clearance delays?

No. EU IOSS itself does not cause delays. IOSS is a VAT reporting mechanism.

Delays typically arise from misclassified e-commerce goods, customs data mismatches, or tariff classification errors between the import declaration, ICS2 filing, and IOSS VAT records. The disruption is data-driven, not VAT-driven.

What is IOSS in a customs declaration context?

In practical terms, an IOSS customs declaration is a standard import declaration that references a valid IOSS number to confirm VAT has already been collected.

Customs authorities still assess HS codes, CN codes, tariff sub-headings, and origin data independently. IOSS does not override customs validation logic.

Why do IOSS EU imports trigger import declaration rejection?

Import declaration rejection often results from:

- HS code errors in EU filings

- CN code misclassification

- Incorrect 8-digit CN or 10-digit tariff code usage

- Customs data mismatch between ENS and declaration

- SKU-level classification inconsistencies

The issue is classification governance, not the IOSS VAT mechanism.

How do tariff classification errors multiply duty under EU low-value imports?

Under the interim rule, the €3 charge applies per tariff sub-heading.

If goods are incorrectly split across multiple 8-digit CN codes or 10-digit tariff codes, duty exposure increases. A shipment that should attract one €3 charge may incur €6 or €9 due to classification inconsistency, not product value.

What causes customs risk referral under ICS2 data validation?

ICS2 data validation compares pre-arrival security data with the formal import declaration.

Where inconsistencies exist, for example, between HS codes in the ENS filing and the final declaration, customs systems may flag the shipment for risk referral or secondary validation, even if IOSS VAT was correctly applied.

Why are misclassified e-commerce goods becoming a bigger issue after 1 July 2026?

Because EU low-value imports are moving from simplified treatment to structured enforcement.

The €3 per tariff sub-heading rule and upcoming EU Customs Data Hub increase visibility of:

- SKU-level classification variance

- Import declaration discrepancies

- Repeated customs data validation failures

Errors that were previously minor become cumulative risk factors.

What is product classification governance in cross-border e-commerce compliance?

Product classification governance refers to consistent, structured assignment of HS and CN codes across all filings, platforms, and jurisdictions.

Without governance, high-volume sellers generate:

- Import declaration discrepancies

- Customs clearance delays in the EU

- Elevated customs audit risk

Classification is now a systemic control function, not an administrative afterthought.

Does having an IOSS number eliminate customs compliance risk?

No. An IOSS number confirms VAT has been accounted for. It does not eliminate exposure related to:

- HS code errors in EU filings

- CN code misclassification

- Tariff sub-heading inconsistencies

- Customs data mismatch across systems

IOSS solves VAT friction. It does not solve data integrity failures.

You may also like:

Struggling to Extract, Catagorise & Validate Your Documents?

Capture & Upload Data in Seconds with AI & Machine Learning

Subscribe to our Newsletter

About iCustoms

iCustoms is an all-in-one solution helping businesses automate customs processes more efficiently. With AI-powered and machine-learning capabilities, iCustoms is designed to streamline your all customs procedures in a few minutes, cut additional costs and save time.

Struggling to Extract, Catagorise & Validate Your Documents?

Capture & Upload Data in Seconds with AI & Machine Learning